mutual funds can be grouped together in several ways. There is no right or wrong way and each fund portal (Value Research, Morning Star, Money Control etc.) have their own categorisation scheme. (View Highlight)

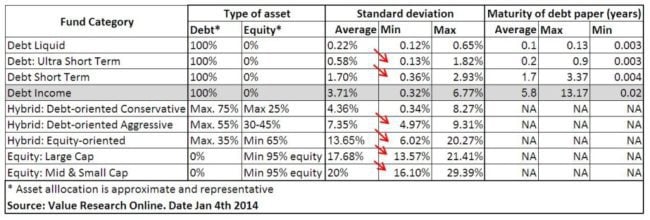

The category standard deviation, along with the typical asset allocation and maturity of debt paper (for debt funds) is listed below for some of the categories define by VR online. (View Highlight)

Category standard deviation refers to the average standard deviation in a particular category. (View Highlight)

• As you go down the table, the equity component increases. Obviously, if a fund has more equity allocation, higher would be the fluctuations in return and therefore higher the category standard deviation. (View Highlight)

The debt income category has different kind of debt funds (dynamic bond funds, diversified debt funds, that is funds that invest in paper that matures over different periods etc.). So it is not an exclusive group. This is why there is a huge variation in standard deviation and average maturity. (View Highlight)

• Liquid debt funds invest in short-term debt paper ranging over a couple of months while income debt funds invest in debt paper that can have an age of several years. (View Highlight)

• It is clear that, higher the age of the maturity, higher is the standard deviation and therefore higher the fluctuations in returns. Of course, this also means higher returns …. typically! (View Highlight)

If I choose a debt income fund that matches with the category average standard deviation of 3.71%,

My returns will typically (68% probability!!) range from

X -3.71% to X+3.71% before taxes!

Can I afford such a swing in returns?

If the answer is no, we can move on and choose somthing with lower standard deviation. What if the answer is yes?!

What if I say, I don’t mind this fluctuation?

Then you will have to worry about what X is, or what it can be.

Let us now introduce a simple but reliable rule of thumb.

• If the return(X) is greater than the corresponding standard deviation (3.70%), there is little or no chance of losing the capital invested.

• If the return is lesser than the corresponding standard deviation, chances of losing the capital invested are high. (View Highlight)

Note: Sure! Let’s consider a fictional Debt Income Fund (Fund A) with a standard deviation of 3.71% which falls under the category average.

Suppose the expected return (X) of Fund A is 7%.

Before investing, you need to decide if you can afford the potential fluctuations in returns. For Fund A, there is a 68% probability that the returns will fall within the range of (X - 3.71%) to (X + 3.71%). So, in this case, the returns can range between (7% - 3.71%) and (7% + 3.71%), which is 3.29% to 10.71%.

Now, based on the rule of thumb mentioned in the previous explanation, since the expected return (7%) is greater than the standard deviation (3.71%), there is a low chance of losing your capital invested.

As an investor, if you can accept the possible fluctuations in returns ranging from 3.29% to 10.71%, then Fund A might be a suitable investment for you. However, if this range is too wide or you cannot afford such a swing in returns, you may want to look for a fund with a lower standard deviation.

for an income fund X should, under normal circumstances, be higher than the standard deviation. (View Highlight)

debts market can crash too (has happened many a time before). That is the NAV of a debt fund can sharply decrease in a day or over the course of a few weeks. (View Highlight)

Longer the average maturity period, higher the corresponding standard deviation and therefore longer the time it would take for the debt fund to recover. (View Highlight)

Higher the standard deviation, bigger would be fall in the event of a crash and therefore longer it would take the debt fund to recover. (View Highlight)

Funds with typical maturity period of more than 1 year are likely to take about 6 months to recover from a crash. (View Highlight)

Debt income funds are well suited only for long term goals (more than 5 years at least). (View Highlight)

Liquid funds over a few days. Short term funds over a couple of months and ulta-short term funds a little earlier that that. (View Highlight)

Therefore, for investment durations of just 1-2 years stick with Short-term/Ultra-short-term/liquid funds. Fixed maturity plans (FMP) are also a good option for such durations. (View Highlight)

For durations less than or equal to 5 years, the power of compounding is not that important. Therefore inflation is not that important. So I will prefer to safeguard the capital, choose debt funds of low risk. (View Highlight)

Why not RDs or Bank FDs? If the goal is crucial and I know exactly how much I need, I will use these even if I fall in the 30% slab. If the goal is less important, then low-risk debts offer a tax advantage. (View Highlight)

Debt income funds that invest in debt paper of short duration with low standard deviation. (View Highlight)

Note: Invest durations between 5-10 years

Debt-oriented Hybrid-funds with about 20-30% equity . Debt portfolio should have low maturity duration. Equity folio should have a good amount of large cap stocks. (View Highlight)

(View Highlight)

(View Highlight)